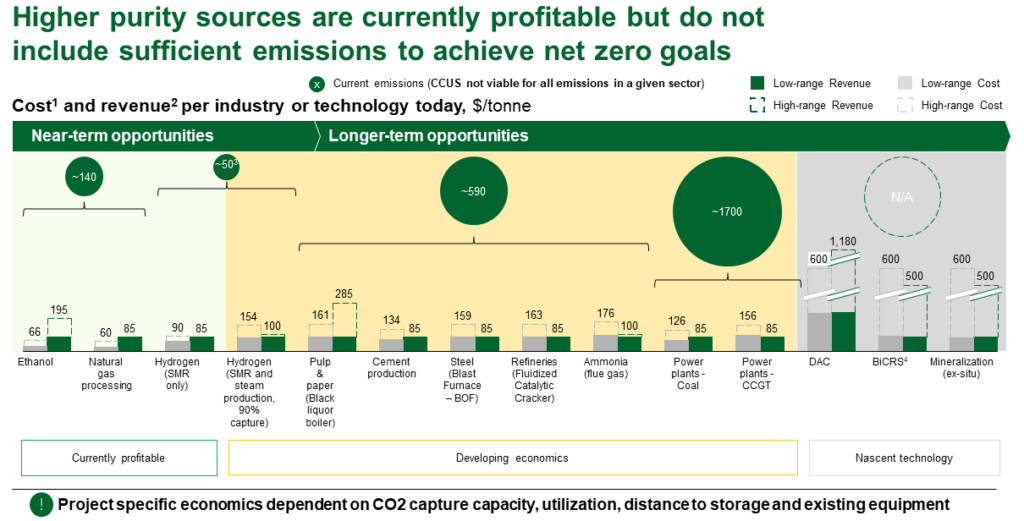

Displayed cost estimates based on EFI Foundation capture costs with transport (GCCSI, 2019) and storage (BNEF, 2022) costs of ~$10-40/tonne, except where noted. All in 2022 dollars. All CCUS figures represent retrofits, not new-build facilities. The lower bound costs represents a NOAK plant in a low cost retrofit scenario with low inflation. The higher bound costs represents a FOAK plant in a high cost retrofit scenario with high inflation. The inflation variance on each cost estimate represents the range of cost increases on a generic chemical processing facility due to inflation from 2018 using the Chemical Engineering Plant Cost Index (CEPCI).

Revenues based on applicable mix of 45Q tax credit, Low Carbon Fuel Standard, Voluntary Carbon Markets and the 45V tax credit (which cannot be stacked with 45Q). Other sources of revenue (e.g., premium PPAs, EOR) are discussed in more detail in the appendix. Tax credit values do not reflect expected discounts to the face value of the credit associated with tax equity financing or transferability. For retrofits, revenue does not reflect the value of products already sold by the facility (e.g., electricity from an existing power plant)

Current hydrogen capacity is likely to grow with the growth of reformation-based capacity and future demand likely

Includes BECCS to power, biochar, and bio-oil; Biochar and bio-oil may not be eligible for 45Q

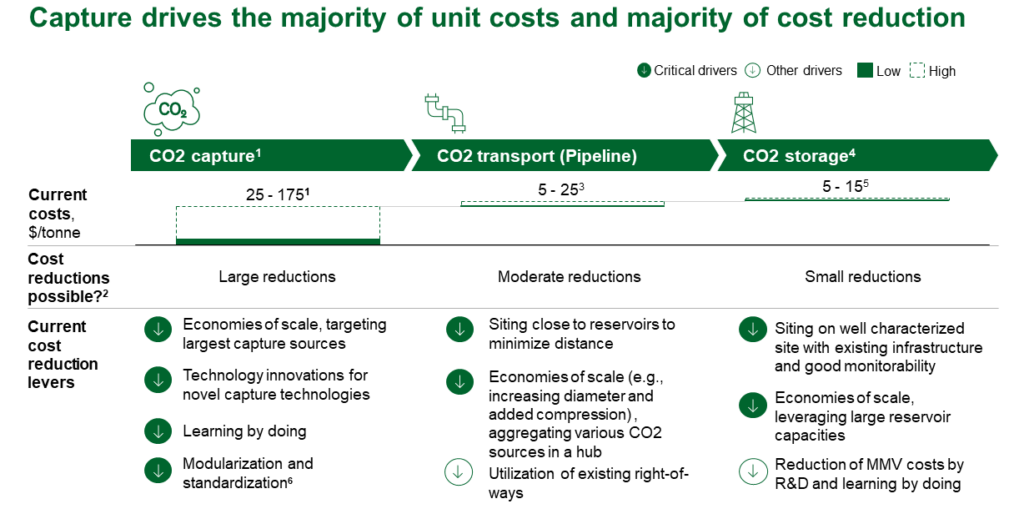

Refers to CO2 capture broadly across sectors examined in this report (see Figure 1); Costs drawn from EFI Foundation, “Turning CCS Projects in Heavy Industry & Power into Blue Chip Financial Investments”

Refers to CO2 capture broadly across sectors examined in this report (see Figure 1); Costs drawn from EFI Foundation, “Turning CCS Projects in Heavy Industry & Power into Blue Chip Financial Investments”

Generalized across sectors. Individual sectors will have sector-specific cost reductions

Approximate costs based on published studies by the European Zero Emission Technology and Innovation Platform, the National Petroleum Council, and GCCSI process simulation for a 30 year asset life. All costs have been converted to a U.S. Gulf Coast basis. Lower end of pipeline cost assumes 20 MTPA, 180 km onshore pipeline. Upper end of pipeline cost assumes 1 MTPA, 300 km onshore pipeline.

Utilization routes also exist including, but not limited to, conversion of CO2 into synfuels or plastics and utilization of CO2 in EOR and building materials

Figure represents a levelized cost of site screening, site selection, permitting & construction, operations, and site closure and post-injection site care

Modularization will be a more critical driver for certain technology types than for others